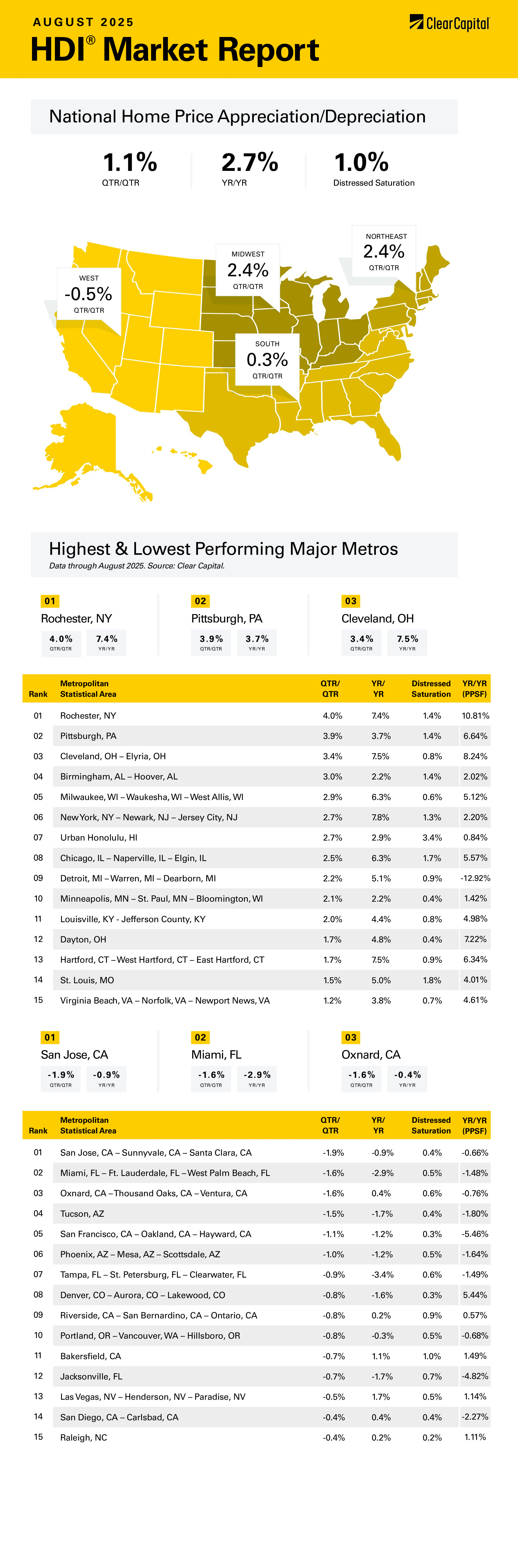

The August 2025 Clear Capital Home Data Index (HDI®) Market Report shows national quarter-over-quarter home price growth is at 1.1 percent.

Download the report, or read it below.

Commentary by Brent Nyitray of The Daily Tearsheet

Home price appreciation continued to slow in August, according to the Clear Capital Home Data Index. National home prices rose 1.1% on a quarterly basis and 2.7% annually. The Northeast and the Midwest continue to outperform, while the West and the South lag behind the rest of the US.

The Northeast was the top-performing market on a quarterly annual basis, rising 2.4% quarterly and 6.3% annually. The top Northeastern metropolitan statistical area (MSA) was once again Rochester, NY, where prices rose 4.0% on a quarterly basis and 7.4% annually. The New York City area saw strong growth, rising 2.7% on a quarterly basis and 7.8% annually. Hartford, CT, also performed well, rising 1.7% quarterly and 7.5% on an annual basis. Despite the high numbers, these MSAs declined relative to July.

The Midwest was the next-best performer, with prices rising 2.4% on a quarterly basis and 4.8% annually. Cleveland, OH was the top performer, with prices rising 3.4% on a quarterly basis and 7.5% on an annual basis. Milwaukee saw prices rise 2.9% on a quarterly basis and 6.3% on an annual basis. Chicago was a top performer as well, with prices rising 2.5% on a quarterly basis and 6.3% on an annual basis.

The South came in third, where prices rose 0.3% on a quarterly basis and 0.8% on an annual basis. Birmingham, AL was the top performer, with prices rising 3.0% on a quarterly basis and 2.2% annually. Miami was one of the worst performing MSAs in the South, with prices falling 1.6% quarterly and 2.9% annually. Tampa, FL also struggled with prices falling 0.9% on a quarterly basis and 3.4% annually.

The West came in last, where prices fell 0.5% on a quarterly basis and rose only 0.5% annually. The only Western MSA to hit the top 15 was Honolulu where prices rose 2.7% quarterly and 2.9% annually. The worst performing MSA was San Jose, CA, where prices fell 1.9% on a quarterly basis and 0.9% on an annual basis. Phoenix also struggled, with prices falling 1.1% on a quarterly basis and 1.2% on an annual basis.

Home price appreciation continues to moderate according to every real estate index out there. The Clear Capital Home Data Index contains more recent data points than the other indices, although they are all saying the same thing. The first-time homebuyer is in an unenviable position, with elevated home prices and a softening job market. Inventory remains tight largely due to the rate lock-in effect, which is due to the differential between current mortgage rates and historical ones. Older empty-nesters who would be amenable to moving into a cheaper lower-maintenance condo are finding that the savings are minimal given that they are giving up a 3.5% mortgage rate for a 6.5% one.

Relief is probably on the way, however, as mortgage rates have been decreasing both on an absolute basis and versus Treasuries. Since the beginning of the year, mortgage rates have fallen from just over 7.05% to just about 6.55%. The markets think the Fed is going to cut rates in September and December so rates should move lower into the end of the year.

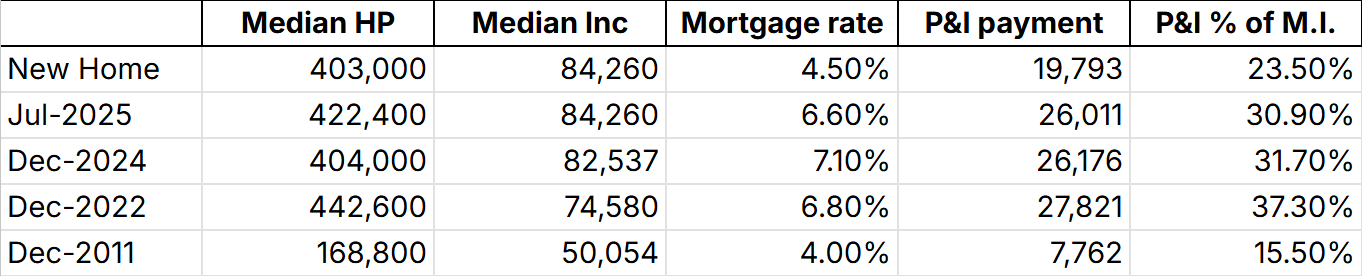

Affordability is improving. At the end of 2024, the median home price was roughly $404,000 and the median income (per Motio research) was $82,500. Today, the median home price is $422,400 and the median income is $84,300. At first glance, it doesn’t look like a big deal: house prices are up and so are incomes. That said, mortgage rates are lower and that matters. At the end of last year, the mortgage payment on that house (assuming 20% down) would consume 31.7% of median income. Today, with a 6.55% mortgage, it consumes 30.9%. If mortgage rates hit 6%, then the payment would be just over 29%. So, while a lot of the think pieces about housing in the media focus on median prices and income, they ignore interest rates, which is a key component to the calculation. To put the current numbers into perspective, at the end of 2022 the worst level of home affordability, the median mortgage payment consumed about 37% of income. At the best period of affordability, late 2011, it was 15.5%.

Existing homes aren’t the only game in town. Builders are sitting on inventory and offering below-market rate mortgages to entice people to buy new homes. Some builders are offering 30-year fixed rates of 4.5% or 5% to move the merchandise. Why are they doing this? Builders would rather cut mortgage rates than cut home prices because they want to maintain the comps in a new neighborhood. They will make more on the house, but they will lose money on the mortgage. The median new home price is 403,000. With a discounted mortgage rate of 4.5%, a buyer can get into a new home for 23.5% of median income. New homes are rarely cheaper than existing homes, but that is the case today.

Below is a table of the scenarios:

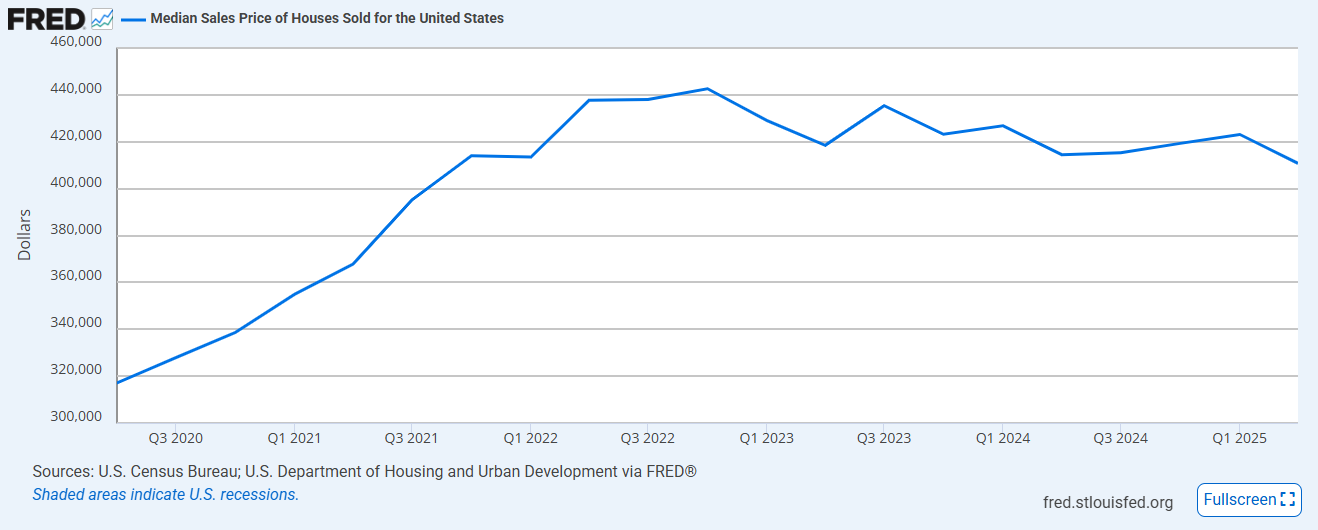

Please note that I am using median home prices here, which are comparable to home price indices since product mix affects the numbers. Starter homes are hot, while McMansions are not, which lowers the median sales price. So, while the real estate indices are still hitting record highs, the median home price has been declining since peaking in 2022:

As home price appreciation continues to moderate, shelter inflation will become a drag on the inflation indices. While we don’t know exactly how tariffs will push up inflation, declining shelter inflation will help push rates lower, thus helping the affordability issue even more. We could be entering a virtuous cycle for the housing market provided tariff inflation doesn’t dramatically worsen.

About the Clear Capital Home Data Index (HDI®) Market Report and Forecast

The Clear Capital HDI Market Report and Forecast provides insights into market trends and other leading indices for the real estate market at the national and local levels. A critical difference in the value of Clear Capital’s HDI Market Report and Forecast is the capability to provide more timely and granular reporting than nearly any other home price index provider.

Clear Capital’s HDI Methodology

• Generates the timeliest indices in patent pending, rolling quarter intervals that compare the most recent four months to the previous three months. The rolling quarters have no fixed start date and can be used to generate indices as data flows in, significantly reducing multi-month lag time that may be experienced with other indices.

• Includes both fair market and institutional (real estate owned) transactions, giving equal weight to all market transactions and identifying price tiers at a market specific level. By giving equal weight to all transactions, the HDI is truly representative of each unique market.

• Results from an address-level cascade create an index with the most granular, statistically significant market area available.

• Provides weighted repeat sales and price-per-square-foot index models that use multiple sale types, including single-family homes, multi-family homes and condominiums.

The information contained in this report and forecast is based on sources that are deemed to be reliable; however, no representation or warranty is made as to the accuracy, completeness, or fitness for any particular purpose of any information contained herein. This report is not intended as investment advice, and should not be viewed as any guarantee of value, condition, or other attribute.