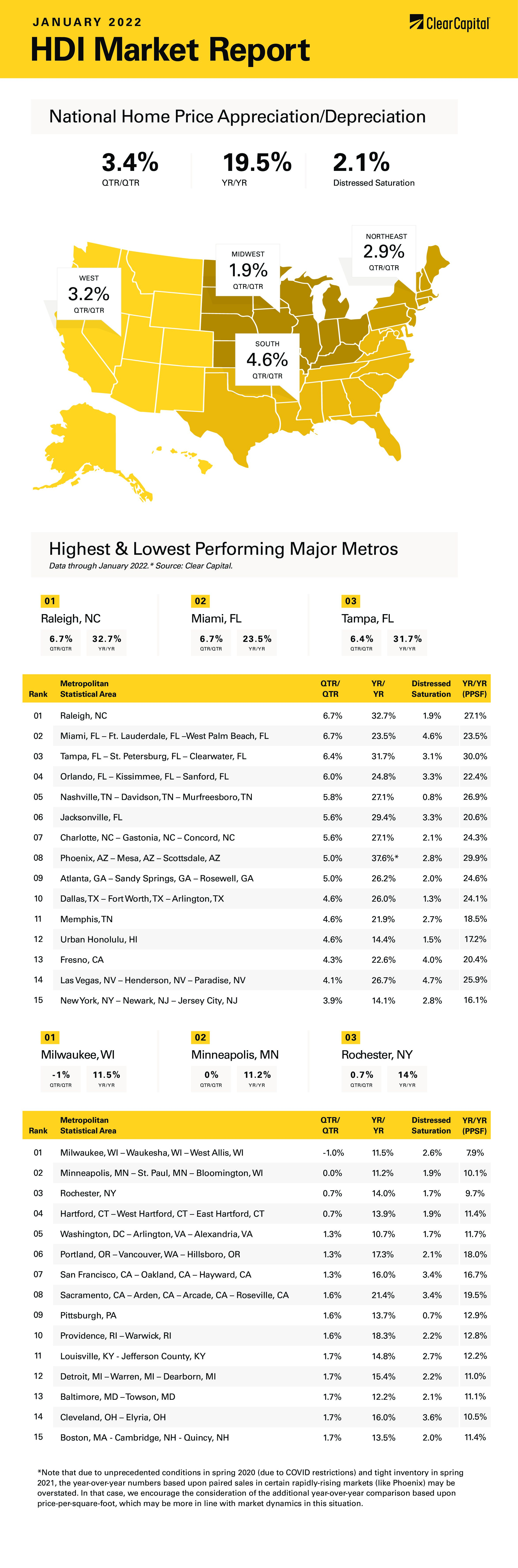

The January 2022 Home Data Index™ (HDI™) Market Report shows national quarter-over-quarter (QoQ) home price growth is at 3.4 percent.

Download the report, or read it below.

* Note that due to unprecedented conditions in spring 2020 (due to COVID restrictions) and tight inventory in spring 2021, the year-over-year numbers based upon paired sales in certain rapidly-rising markets (like Phoenix) may be overstated. In that case, we encourage the consideration of the additional year-over-year comparison based upon price-per-square-foot, which may be more in line with market dynamics in this situation.

Commentary by Brent Nyitray of The Daily Tearsheet

Home price appreciation continued last month as the Clear Capital Home Data Index rose 3.4% quarter-over-quarter (QoQ) and 19.5% on a year-over-year (YoY) basis. This was a slight deceleration from the December pace of 3.9% quarter-over-quarter and 19.9% YoY. Every region reported home price appreciation, and some of the hottest markets like Phoenix are coming back down to Earth. We are also seeing the fastest-growing metropolitan statistical areas (MSAs) concentrated in a few states. Florida remains one of the strongest states overall, taking 3 of the top 5 MSAs.

The fastest growing region remains the west, which grew 23% last month. Again, Phoenix was the leader, with prices rising 38% on a YoY basis, compared to 39% last month. On a price-per-square foot basis, prices rose 30%. Other notable western MSAs include Las Vegas, where prices rose 27% and Fresno, where they rose 23%.

The south came in second at 22%, with a slew of metropolitan statistical areas in the top ten. North Carolina did will, with Raleigh real estate rising 33% and Charlotte rising 27%. Florida had a slew of leaders, including Miami (up 24%), Tampa (up 32%), Orlando (up 25%) and Jacksonville (up 29%).

The Northeast came in next, where prices rose 16% on a year-over-year basis. One of the biggest laggards has been the New York City area, which has been battered by job losses in finance. Things may be turning around there, as prices rose 14% YOY, however they were up 3.9% on a quarter-over-quarter basis. Boston saw prices rise 14% as well.

Finally, the Midwest saw a 16% increase in prices. Since the top 15 MSAs were dominated by the South and West, no Midwestern MSAs made the list. The slowest MSA went to Milwaukee, where prices fell on a quarterly basis, but were still up 12% year-over-year. Minneapolis was also a laggard, with prices flat on a quarter-over quarter basis and rising 11% annually.

The Federal Reserve maintained the current level of interest rates at the January FOMC meeting but set the stage for rate hikes starting in March. The Fed has been buying Treasuries and mortgage-backed securities since the early days of the COVID-19 pandemic, and it looks like the Fed will try and unwind the buildup going forward.

There was an interesting statement in the Fed’s Principles for Reducing the Size of the Federal Reserve’s Balance Sheet: “In the longer run, the Committee intends to hold primarily Treasury securities in the SOMA, thereby minimizing the effect of Federal Reserve holdings on the allocation of credit across sectors of the economy.”

This statement regarding “minimizing the effect of Federal Reserve holdings on the allocation of credit” seems to be an admission that the housing market has increased in value much faster than the Fed would like. The Federal Government has spent $5.7 trillion in COVID-19 relief, and the Federal Reserve has bought $4.8 trillion worth of Treasuries and mortgage-backed securities. This is an enormous amount of stimulus, and it helped drive the 20% increase in home values last year, as well as the big increase in the stock market.

As the Fed prepares to take away the punch bowl, stock market valuations have started to decrease, and residential real estate analysts are taking down their estimates for 2022 home price appreciation. Freddie Mac is forecasting home price appreciation to slow to 6.2% in 2022 and fall even further to only 2.5% in 2023.

Ultimately, the driver of home price appreciation will be the supply and demand picture. The National Association of Realtors reported that home inventory hit a record low in December – only 910,000 units, which represents 1.8 months’ worth of inventory at the current pace. To put that into perspective, six months is roughly a balanced market. With lumber prices again above $1,000 and a shortage of skilled labor, new construction is expected to be limited and expensive. While the Fed’s actions will probably take some froth off the housing market, residential real estate is still one of the go-to assets in an inflationary environment as it generally will outperform other assets like stocks and bonds.

Speaking of inflation, the GDP report showed the economy growing at a brisk 6.9% pace, which historically would be considered a massive boom. That said, the mood of consumers isn’t really reflecting that, and the economy doesn’t feel like, say the late 1990s. The report gives a possible explanation why: Real disposable personal income declined 5.8% in the fourth quarter, which means that wages aren’t keeping up with inflation.

This could present a problem to the Fed, especially if the big fourth quarter numbers were being driven by stimulus which is now fading. The Fed must manage both unemployment and inflation, and it risks softening the labor market to tackle inflation. The next several months will be challenge for the central bank.

About the Clear Capital Home Data Index™ (HDI™) Market Report and Forecast

The Clear Capital HDI Market Report and Forecast provides insights into market trends and other leading indices for the real estate market at the national and local levels. A critical difference in the value of Clear Capital’s HDI Market Report and Forecast is the capability to provide more timely and granular reporting than nearly any other home price index provider.

Clear Capital’s HDI Methodology

• Generates the timeliest indices in patent pending, rolling quarter intervals that compare the most recent four months to the previous three months. The rolling quarters have no fixed start date and can be used to generate indices as data flows in, significantly reducing multi-month lag time that may be experienced with other indices.

• Includes both fair market and institutional (real estate owned) transactions, giving equal weight to all market transactions and identifying price tiers at a market specific level. By giving equal weight to all transactions, the HDI is truly representative of each unique market.

• Results from an address-level cascade create an index with the most granular, statistically significant market area available.

• Provides weighted repeat sales and price-per-square-foot index models that use multiple sale types, including single-family homes, multi-family homes and condominiums.

The information contained in this report and forecast is based on sources that are deemed to be reliable; however, no representation or warranty is made as to the accuracy, completeness, or fitness for any particular purpose of any information contained herein. This report is not intended as investment advice, and should not be viewed as any guarantee of value, condition, or other attribute.