West and Northeast tied for most March growth, California Dominates Top 15 Performing MSAs

Nationally, quarter-over-quarter (QoQ) home price growth increased slightly to one percent, up 0.1 percent from February. Clear Capital’s patent-pending QoQ measurement uses the newest data to create timely indices in rolling quarter intervals, which significantly reduces multi-month lag time that may be experienced with other indices.

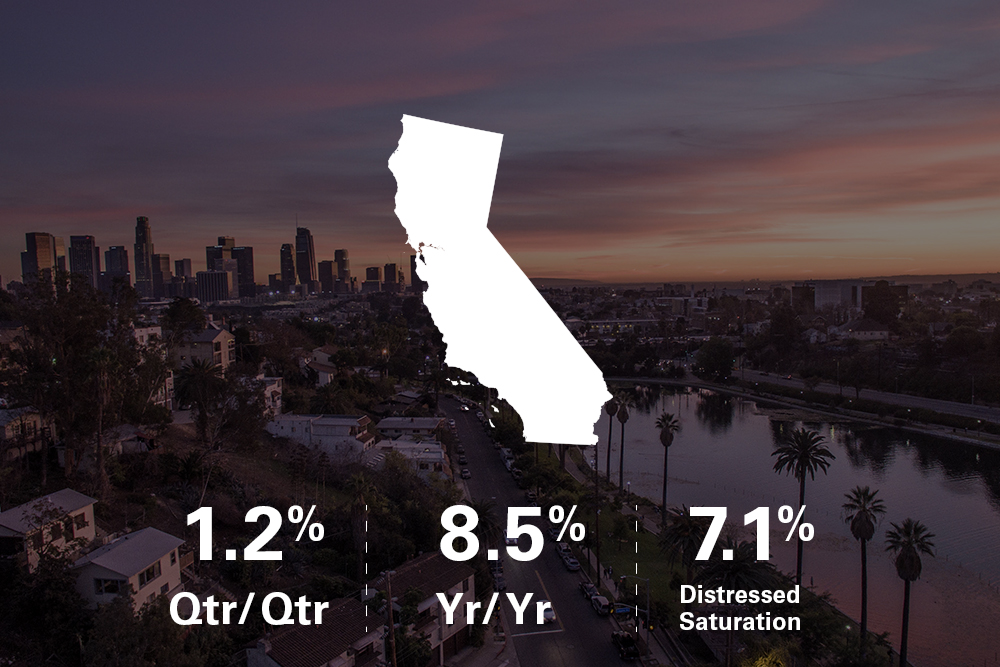

West Region

The West continues strong regional growth with 1.2 percent QoQ growth for March, up 0.1 percent from the previous month.

Las Vegas and San Jose, California continue as top nationwide performers with 2.08 percent and 1.83 percent QoQ price growth, respectively. In addition, five other western cities are among the top 15 highest nationwide performers:

- Seattle, Washington: 1.52 percent growth

- Riverside, California: 1.50 percent growth

- Los Angeles, California: 1.31 percent growth

- San Diego, California: 1.27 percent growth

- Sacramento, California: 1.24 percent growth

Oxnard, California saw improvements for March, up 0.26 percent to 0.85 percent QoQ growth. Honolulu dropped significantly with 0.01 percent QoQ growth, down 0.59 percent from February.

Northeast Region

The Northeast maintains its pressure on the West with growth of 1.2 percent QoQ growth for March. Notable performers in the region included:

- Providence, Rhode Island fell from February’s high and is down 0.29 percent to 1.77 percent QoQ growth for March.

- New York, New York slid down with 1.12 percent QoQ growth, knocking it out of the top 15 nationwide performers.

- Philadelphia, Pennsylvania saw gains for March, up 0.06 percent to 0.64 percent QoQ growth.

- Rochester, New York fell sharply for March, down 0.27 percent from the previous month and settled in at 0.64 percent QoQ growth.

- Pittsburgh, Pennsylvania saw a moderate increase with 0.23 percent QoQ growth, up 0.17 percent, but is still ranked at the bottom of the top 15 worst nationwide performers.

South Region

The South is up slightly to 0.8 percent QoQ growth, improving 0.1 percent from February.

Memphis, Tennessee maintains its strong performance with 1.59 percent QoQ growth, up 0.14 percent. Dallas was able to surpass Memphis, Tennessee with an increase in QoQ growth of 0.24 percent to reach 1.63 percent. New Orleans was able to reserve a spot amongst the top 15 nationwide performers with QoQ growth of 1.31 percent.

Among the South’s worst performers:

- Richmond, Virginia grew 0.25 percent to 0.96 percent

- Orlando, Florida grew 0.11 percent to 0.88 percent

- Raleigh, North Carolina grew 0.08 percent to 0.79 percent

- Virginia Beach, Virginia grew 0.03 percent to 0.48 percent

Houston remained the same with 0.77 percent QoQ growth. Birmingham, Alabama (0.42 percent), and San Antonio (0.25 percent) all experienced negative growth for March, at 0.07 percent and 0.13 percent respectively.

Midwest Region

The Midwest also experienced slight growth for March, up 0.1 percent to 1.0 percent QoQ growth.

Detroit faltered in March with QoQ growth of 1.34 percent, down 0.39 percent from February. Additionally, Dayton, Ohio (2.05 percent), Cleveland (1.60 percent), and Columbus, Ohio (1.35 percent) experienced significant gains of 0.58 percent, 0.17 percent, and 0.14 percent, respectively.

The Midwest also had some poor performers as well with Louisville, Kentucky being the worst performer of the Midwest at 0.61 percent QoQ growth up 0.07 percent from February. Minneapolis (0.80 percent) and Milwaukee (0.68 percent) were also amongst the bottom 15 nationwide.

About the Clear Capital® Home Data Index (HDI) Market Report

About the Clear Capital® Home Data Index (HDI) Market Report

The Clear Capital HDI Market Report provides insights into market trends and other leading indices for the real estate market at the national and local levels. A critical difference in the value of the HDI Market Report is the capability of Clear Capital to provide more timely and granular reporting than nearly any other home price index provider.

Clear Capital® HDI Methodology

- Generates the timeliest indices in patent pending rolling quarter intervals that compare the most recent four months to the previous three months. The rolling quarters have no fixed start date and can be used to generate indices as data flows in, significantly reducing the multi-month lag time experienced with other indices.

- Includes both fair market and institutional (real estate owned) transactions, giving equal weight to all market transactions and identifying price tiers at a market specific level. By giving equal weight to all transactions, the HDI is truly representative of each unique market.

- Results from an address-level cascade create an index with the most granular, statistically significant market area available.

- Provides weighted repeat sales and price-per-square-foot index models that use multiple sale types, including single-family homes, multi-family homes, and condominiums.

The information contained in this report is based on sources that are deemed to be reliable; however no representation or warranty is made as to the accuracy, completeness, or fitness for any particular purpose of any information contained herein. This report is not intended as investment advice, and should not be viewed as any guarantee of value, condition, or other attribute.